Category: Map of the Month

March Map of the Month

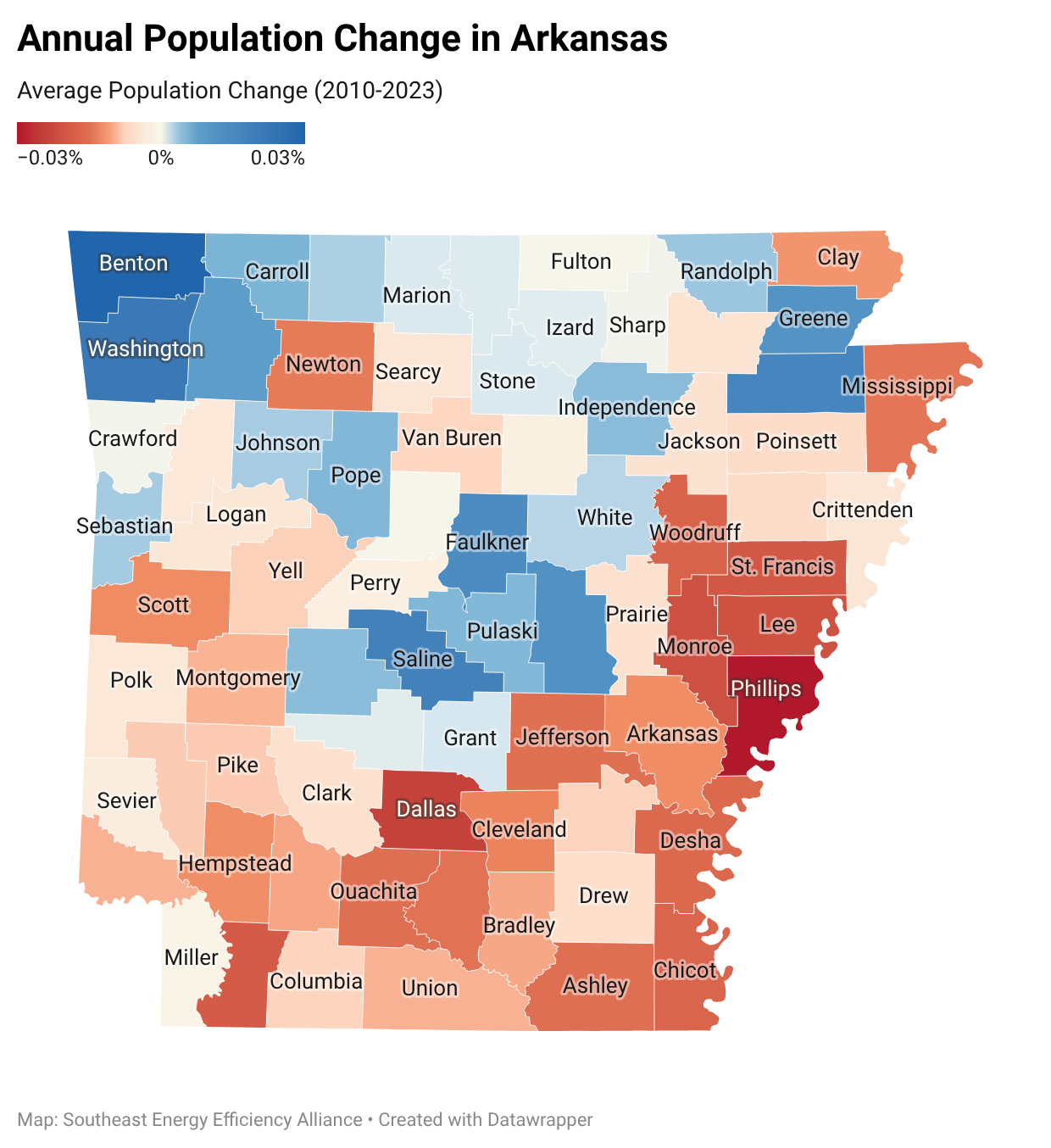

Growth and Energy Burden in Arkansas: A County Comparison

By Laura Diaz-Villaquiran

Data: U.S. Census Bureau ACS (2020–2024); U.S. Energy Information Administration (EIA); U.S. Department of Energy LEAD Tool

Across Arkansas, patterns of population change and energy burden are closely connected. The state consumes nearly 60% more energy than it produces, and while its electricity prices are among the ten lowest nationally, affordability varies widely depending on income, housing quality, and local economic conditions. For many low-to-moderate income households, energy costs still represent a significant share of monthly expenses.

This analysis examines how population change intersects with energy burden statewide. Communities experiencing growth generally benefit from newer housing stock, active labor markets, and expanded economic opportunity factors associated with lower energy costs relative to income. Declining communities, by contrast, often contend with shrinking economies, aging and inefficient housing, and elevated energy burdens that compound existing hardship.

A Tale of Two Counties:

In Arkansas, Benton County and Phillips County illustrate these differences. Benton County, located in northwest Arkansas, has experienced sustained growth, with a population increase of 17% between 2020 and 2025. This growth is supported by a strong labor market, with employment increasing by 7.1% between 2022 and 2023, and significant residential development, with 4,453 building permits issued in 2024.

Benton County also has a more diverse population, with 12.7% foreign-born residents and 15.8% of households speaking a language other than English at home. In Benton, the median household income is $93,506. Homeownership is relatively high at 67%, and 94.4% of households have broadband access. Median monthly housing costs include $1,717 for owners with a mortgage and $1,277 for renters.

Phillips County, located in the Mississippi Delta, presents a different picture. The county experienced a population decline of 13.7% over the same period, alongside a 5.2% decline in employment between 2022 and 2023 and only 16 building permits issued in 2024.

Phillips County is 61.8% Black, 34.5% White, and 2.5% Hispanic or Latino, with a much smaller foreign-born population than Benton County (1.5%).

In Phillips County, the median household income is $40,134, and 35.8% of residents live in poverty, over four times the rate of Benton County.

Homeownership stands at 51.2%, and 79.3% of households have broadband access. The median gross rent in Phillips is $737, reflecting lower housing costs but also lower incomes and limited economic opportunity for its residents.

Energy costs represent a disproportionately large share of income for Phillips County residents. Low-to-moderate-income households carry an average energy burden of approximately 12%, double that of Benton County. Energy poverty researchers define energy burdens of 6% to be high and burdens above 10% severe.

These differences underscore deep regional disparities in the Arkansas–Mississippi Delta, where counties such as Ashley, Chicot, Lee, and Mississippi experience a compounding cycle of population loss, elevated poverty, and severe energy burdens.

SEEA’s work focuses on these regional differences by bringing together cross-sector partners to align data, programs, and policy. Insights like these help target energy efficiency investments, inform workforce development strategies, and support solutions that improve affordability and resilience. By connecting data to action, this approach supports more consistent and measurable progress across communities in the Southeast.

February Map of the Month

By Will Bryan

Housing in the Southeast is aging, and the cost of living in it is getting more expensive. As we noted last month, around 40% of housing in the region was built before 1980, when the nation’s first minimum standards for energy efficiency were implemented. For residents of older homes, occupancy can come with an unexpected tax: the high costs of deferred maintenance and inefficiencies, not to mention the health and safety impacts of living in substandard housing.

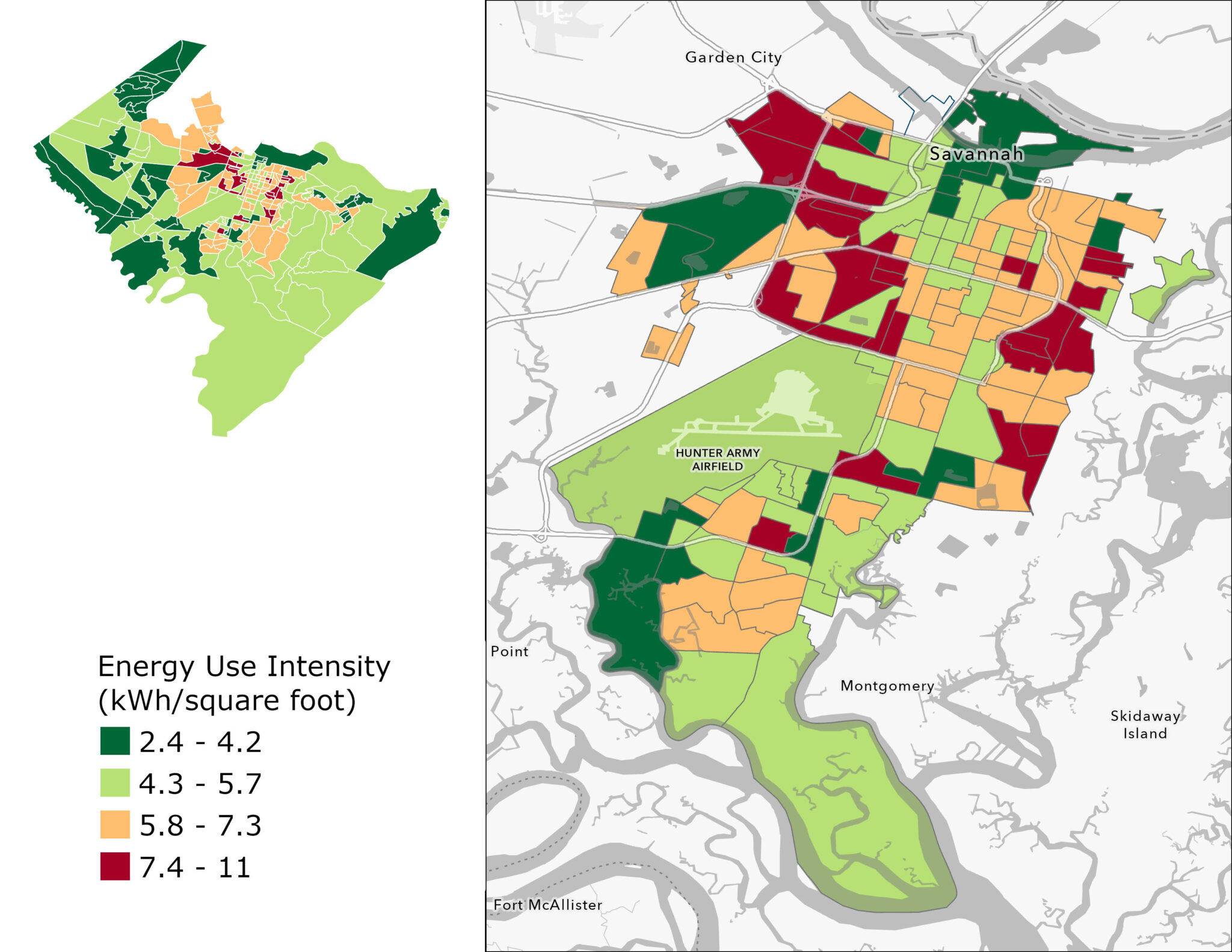

These burdens are not distributed equally. In this month’s map of the month, we assess the quality of housing in Savannah, Georgia using the metric of energy use intensity (EUI), a measure of energy use per square foot. EUI is a helpful proxy for housing quality and efficiency. Higher EUIs signal leaky buildings with heavy heating and cooling loads, while low EUIs indicate more efficient spaces. By modeling heating EUI at the census block group in Savannah, Georgia – a city where the housing stock is older than the state and regional average – we show where efficiency gaps are the widest and shed light on which communities are shouldering the impacts of our aging housing.

As the map shows, EUI varies considerably across the City of Savannah. The most efficient households in the city use more than 4.5 times less energy per square foot than the least efficient households in the city, which translates into considerable monthly cost savings.

The highest EUIs are concentrated on the outskirts of the historic district. While the housing here is nearly as old as that in the city’s core, these neighborhoods have had fewer resources available for retrofits and upgrades. The result is that it is less likely that homes in these areas have been retrofitted and they are more likely to experience the impacts of deferred maintenance.

In Savannah, these issues are shaped by the legacies of the South’s long history of residential segregation. As the chart below indicates, block groups in the city with the highest EUIs all have majority Black populations, while census block groups with the lowest EUIs are all majority white. Additionally, homes in areas with low EUIs tend to be newer than the typical home, benefiting from modern construction techniques and minimum standards for building efficiency. This showcases the ways that segregation, a lack of housing choice, and unequal access to capital over the past century continue to circumscribe who has access to healthy and efficient housing today.

January Map of the Month

Aging Homes, Rising Energy Costs

By Amy Lovell, Ph.D.

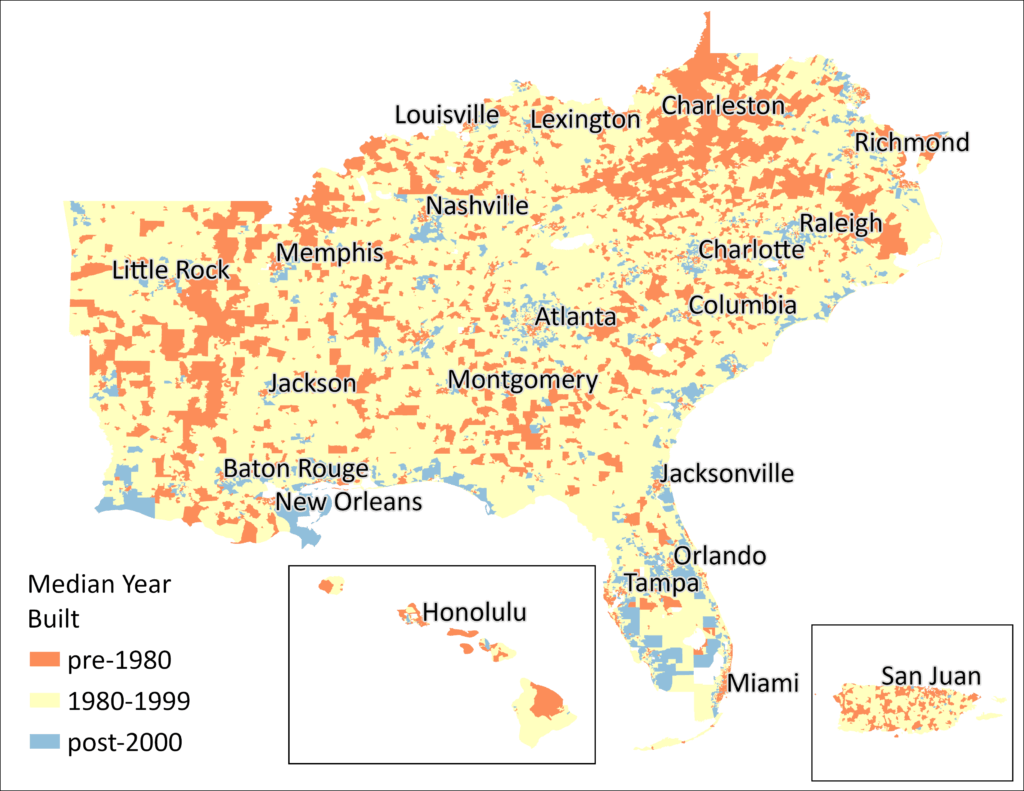

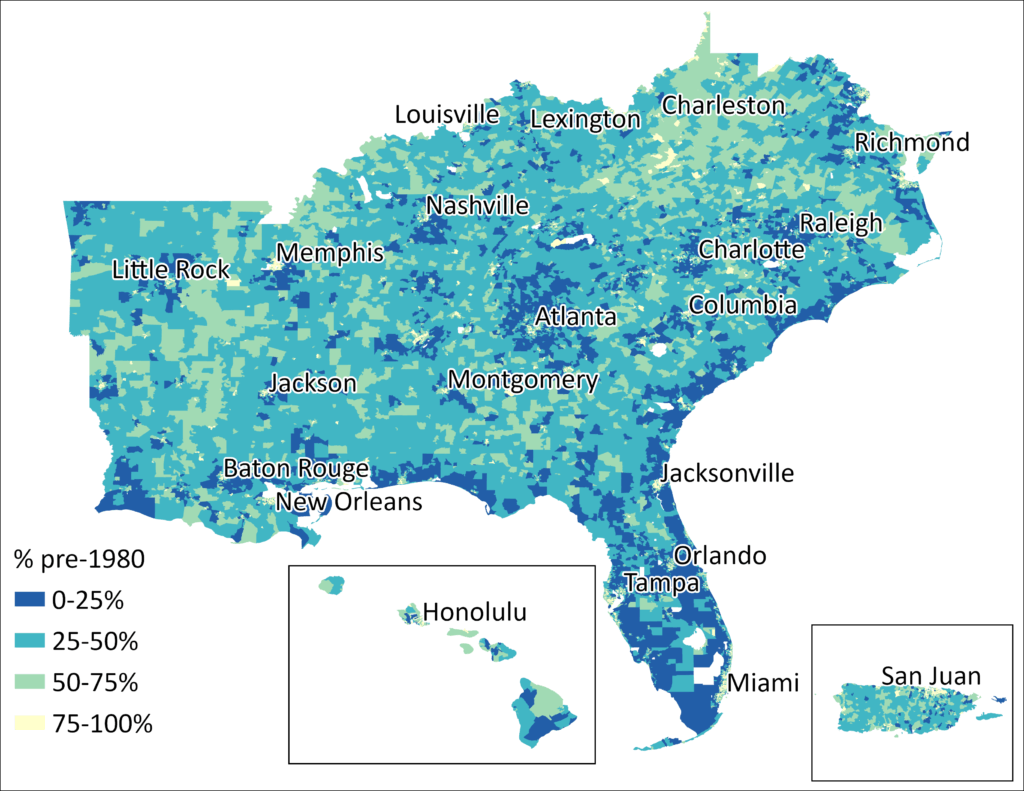

Escalating household energy costs have increased the urgency of energy and housing affordability and drawn attention to the influence of housing characteristics on energy efficiency. Housing age is a major driver of home energy usage and costs, particularly if the home was constructed to lower building standards or is in need of major repairs. In 2020, 27% of households across the U.S. struggled to meet energy needs, and in some areas, that percentage is even higher.

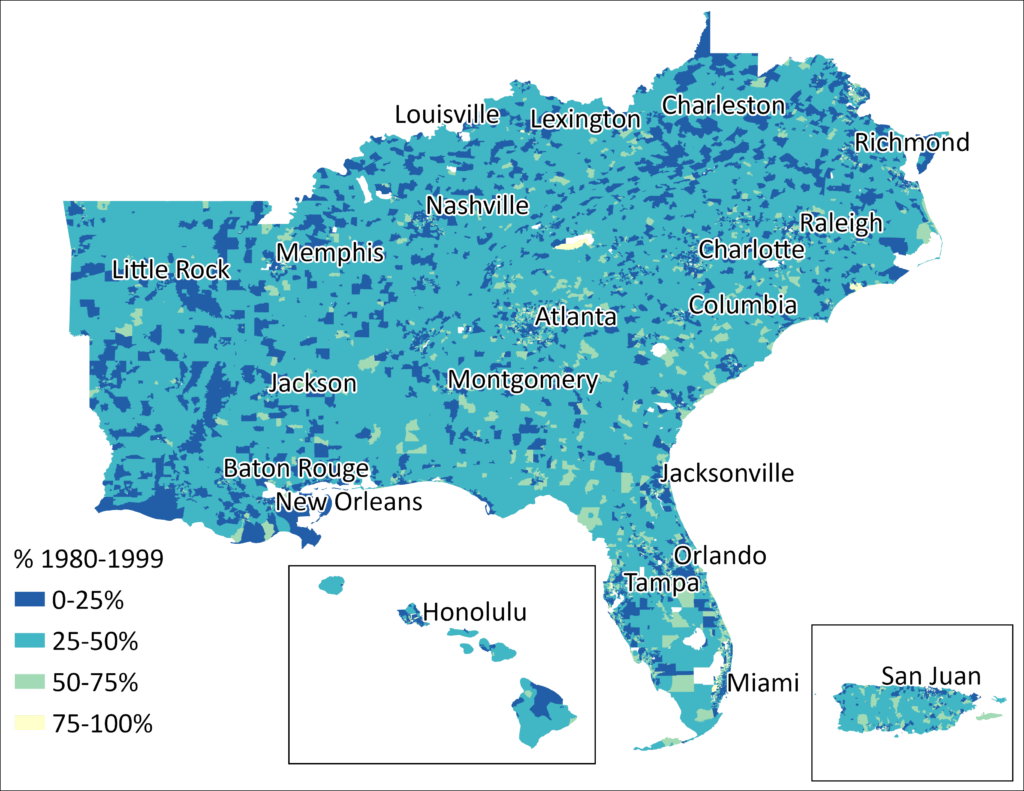

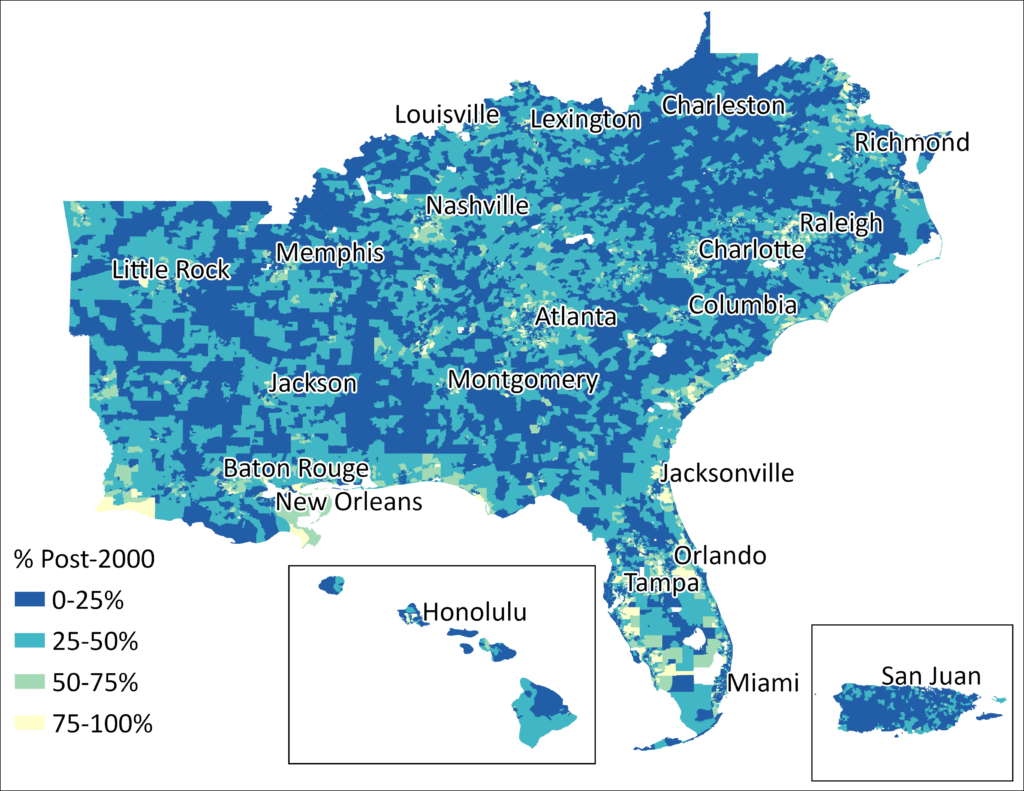

One of the most critical factors influencing the efficiency of housing is the year of construction, as building technologies and code requirements have evolved over time. In the Southeast, approximately 40% of homes were built before 1980, when energy codes started to be required in some jurisdictions nationally. Though only 5% of homes were built in 1939 or earlier, and 14.8% of homes were built before 1960, this still represents 1.9 million and 6 million residences, respectively. Less than 30% of southeastern homes were built after the year 2000.

This month’s map illustrates the percentages of southeastern homes that were built over different time spans, and the median year of construction. Data are estimated at the census tract level, representing 40 million homes in the region, based on the U.S. Census Bureau’s American Community Survey (ACS) from 2023.

Rural areas tend to have a higher proportion of older homes (indicated on the map in darker shades of blue), while areas near cities that have experienced significant growth tend to have a higher proportion of newer homes (indicated in lighter green and yellow). In some rural communities, 40% or more of the homes were first constructed before 1960. Unless those homes have been renovated or had intentional upgrades to energy efficiency, the residents likely experience high energy costs.

For an older home, a comprehensive energy efficiency upgrade – which may include sealing air leaks around doors and windows, adding additional attic or wall insulation, replacing windows or doors, or upgrading heating/cooling systems and thermostats – can save 10-30% on annual energy costs. It is useful for states, counties, and municipalities to know where the majority of residents are living in older homes that could benefit from some attention.

While new construction will typically be built to comply with greater energy efficiency standards, those requirements vary across the region. In Florida, Louisiana, and Virginia, the building energy codes are more favorable to efficient new construction, while in some other states in the region, building standards are 15-20 years behind the most modern standards. The U.S. Department of Energy determined that upgrading building energy codes to the most recent (2024) International Energy Conservation Code (IECC) would result in 7-8% in residential energy savings over the 2021 code, and upgrading older codes holds even greater potential, but only for newly constructed homes.

Older homes may have undergone significant renovations and upgrades to energy efficiency, either as older components were replaced after failure, or in a more comprehensive upgrade targeting energy savings. As a result, many newer homes will operate more efficiently and cost less in annual energy expenditures, but older homes of any age may be much more efficient than others of the same vintage. Home renovation is a major industry, including do-it-yourself and professionally-installed projects (including but not limited to energy upgrades), with total homeowner remodeling spending expected to exceed $500 billion in 2026.

An additional challenge for residents of older homes, particularly for families with limited financial resources, very high energy costs, or significant deferred maintenance projects in the home, is the additional cost of repairing existing damage and preparing the home to benefit from energy efficiency improvements. As increasing energy demand influences household energy costs across the region and the nation, the number of households paying more than 10% of their income on energy bills will continue to grow from the current 12%. National, state, utility, local, and philanthropic funding programs are working to fill these gaps, but in most locations the need greatly exceeds the available funds. For example, SEEA is conducting a pilot program with microgrants to help nonprofits, small businesses, and municipalities who are supporting residents in applying for these programs in five states. States and municipalities can also continue to review and update their building energy codes so that newer housing can operate as efficiently as possible.

November Map of the Month

By Will Bryan

It’s no secret that projected electric loads throughout the nation are unprecedented, but particularly in the Southeast. A recent analysis by ICF estimates that U.S. electricity demand will grow by 25% in the next four years, and 78% by 2050, compared to a 2023 baseline. Much of this load growth will happen in the Southeast, driven by a combination of electrification and the siting of large commercial customers.

Many electric utilities are considering building new generation to manage this unprecedented growth; load flexibility, however, will be a critical tool to maintain grid stability, promote customer affordability, reduce the environmental impacts of generation, and ensure that we have the energy to meet all our needs.

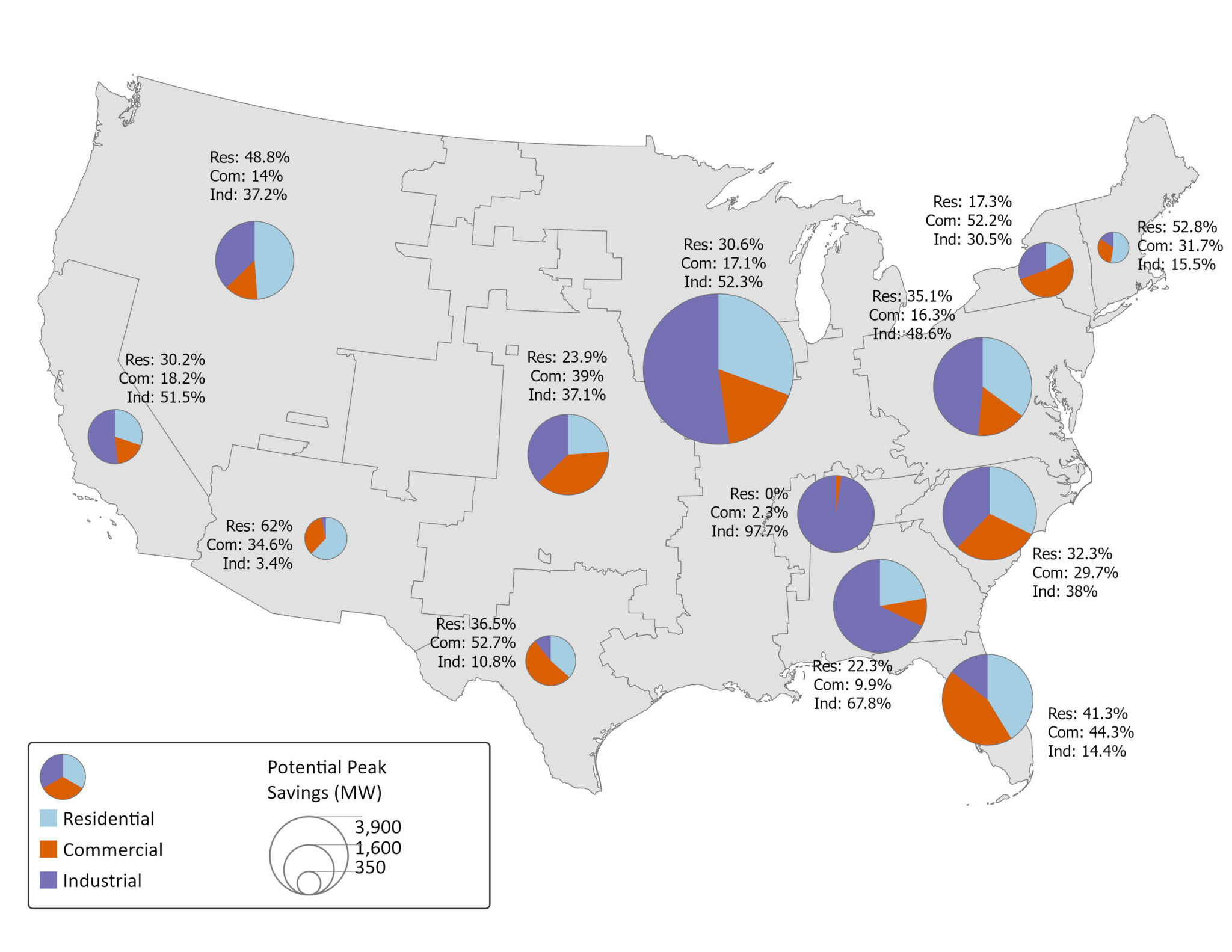

This month’s map uses data from the U.S. Energy Information Administration (EIA) to explore the state of utility-administered demand response programs in 2024, the most recent year data was available. Demand response refers to a range of programs that are designed to reduce customer usage during peak events, including through the installation of smart thermostats or variable pricing, among others.

Utilities of all types have enrolled 2.7 million residential, commercial, and industrial customers in demand response programs across the South. These programs have created the capacity to save approximately 13.34 GW of peak energy use. In 2024, demand response reduced the peak demand by 2.89 GW, the amount of power generated by about three nuclear reactors. Utilities in the Midwest, mid-Atlantic, Carolinas, and Southeast balancing authority regions lead the nation in terms of potential peak capacity reductions available through demand response programs.

As the pie charts in this month’s map show, utilities take different approaches to balancing their programs across multiple sectors. While peak savings in the Southern and Tennessee balancing authority regions are driven largely by the industrial sectors (seen in purple on the pie chart), other parts of the South, such as Florida and the Carolinas, show a greater reliance on residential and commercial demand response approaches.

Demand response is transformational work. It stabilizes the grid during critical events and protects customers from the costs of new infrastructure investment. However, to meet future load projections, these programs must be scaled up rapidly to help meet the projected need.

Expanding demand response offers additional peak-shaving capability, especially when paired with energy efficiency and other distributed energy resources. Demand response is a proven, effective tool. The challenge now is to scale it to meet the emerging demand.

October Map of the Month

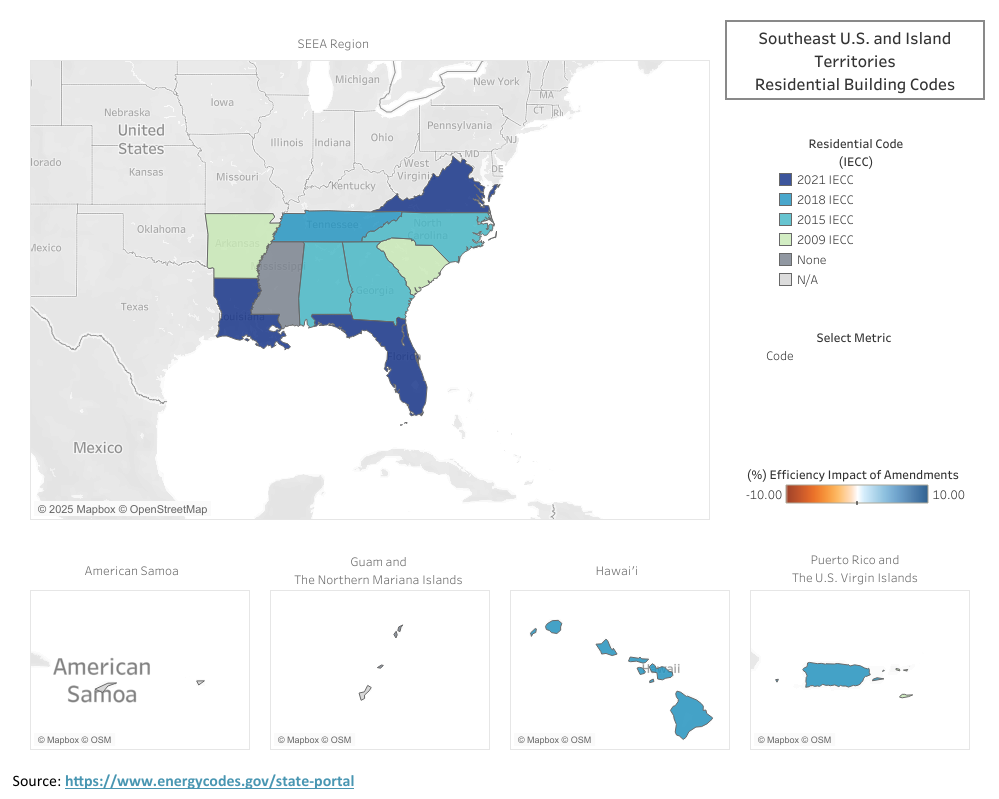

Beyond Adoption: Measuring the Efficiency Impact of State Amendments

Code: The model energy code edition that a state has officially adopted — IECC for residential buildings or ASHRAE Standard 90.1 for commercial buildings.

Strength: The actual rigor of that code after state amendments — shown as the equivalent edition it matches and the percent change in efficiency compared to the unamended base.

Impact (Δ%): The efficiency impact of amendments on the strength of the code — negative values mean the code was weakened, positive values mean it was strengthened.

Code Adoption

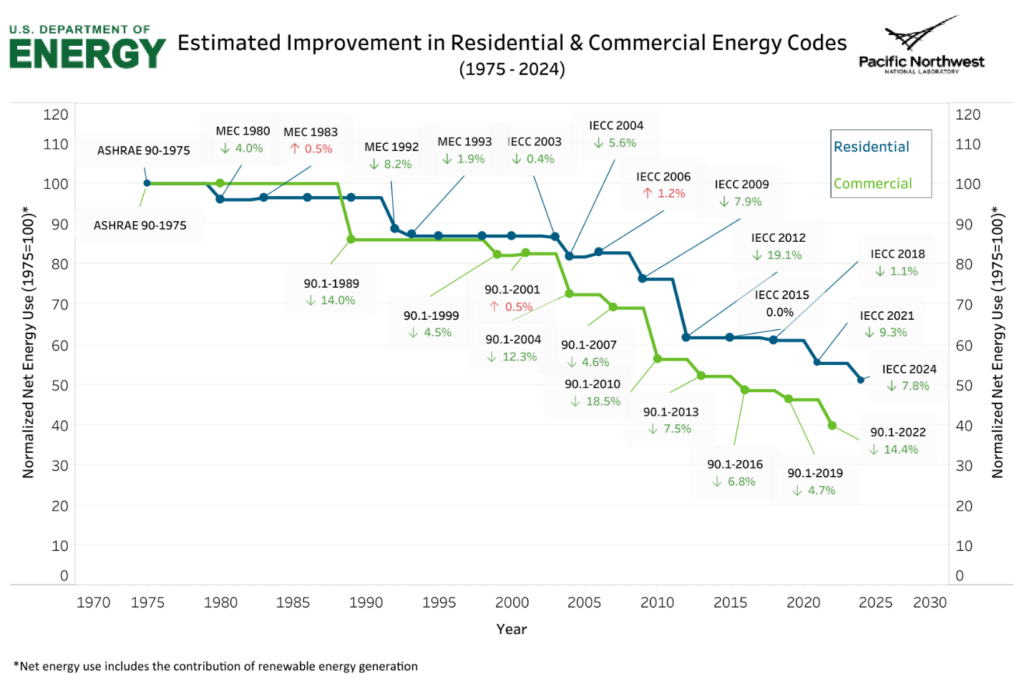

Modern building energy codes were born from the 1970s energy crisis, when the U.S. first recognized the need to make buildings part of the nation’s energy solution. Congress passed the Energy Conservation and Production Act of 1975, prompting ASHRAE to release Standard 90-1975, which was the first model energy standard for both residential and commercial buildings. What began as a response to oil shortages evolved into a national framework for improving efficiency, lowering energy bills, and creating healthier indoor environments.

Today, two model codes define energy performance in new construction: the International Energy Conservation Code (IECC), developed by the International Code Council (ICC), which applies to most low-rise residential buildings; and ASHRAE Standard 90.1, maintained by ASHRAE’s Standing Standards Project Committee 90.1, which governs commercial and multifamily buildings four stories and higher. Both are updated every three years through consensus-based processes that integrate advances in materials, technology, and design.

States adopt these model codes to establish consistent, verifiably effective standards for energy-efficient building design and construction. Using a national model allows jurisdictions to align with proven energy and cost savings while reducing the administrative burden of writing their own code from scratch. Each adoption cycle marks an opportunity to bring new buildings closer to the long-term goals of efficiency, affordability, and resilience.

Amendments

Once a model code is adopted, many states modify it through state-specific amendments that tailor how the code is applied or enforced. Amendments can adjust performance requirements or provisions to accommodate local market or climactic conditions.

States may amend for several reasons: to reflect regional climate, to balance cost and feasibility, or to harmonize with existing state policies. Some strengthen efficiency – tightening envelope requirements or improving lighting and controls – while others weaken it by relaxing testing standards or allowing lower equipment performance.

For example, several states in the Southeast have adopted the 2015 IECC with state-specific amendments, which in effect perform closer to the 2009 IECC. These amendments may often be created to help codes pass politically or reduce near-term costs, but often result in lower long-term energy and health benefits.

Impact of Amendments

On paper, a state’s code might appear to meet a recent national standard. In practice, however, amendments can significantly alter its strength, that is, the actual level of efficiency the code delivers. To capture this nuance, analysts from the U.S. Department of Energy’s Building Energy Codes Program use comparative modeling to estimate how amendments shift a code’s effective performance.

For example, a state that adopts the 2015 IECC but introduces multiple weakening amendments may, in effect, deliver energy savings closer to the 2009 IECC baseline. This map is intended to visualize those distinctions through both Code (what’s on the books) and Strength (what’s actually achieved), offering a clearer view of how policy choices translate into real-world outcomes for efficiency and affordability.

To learn more about the DOE’s State Energy Code modeling methodology, visit the link here.

The Impact (%) represents that estimated difference in energy performance caused by amendments alone – negative values indicate a weaker, less efficient code, while positive values reflect stronger-than-standard performance. Together, these measures show not just what code a state has adopted, but what level of efficiency it’s truly delivering.

September Map of the Month

By Amy Lovell, Ph.D.

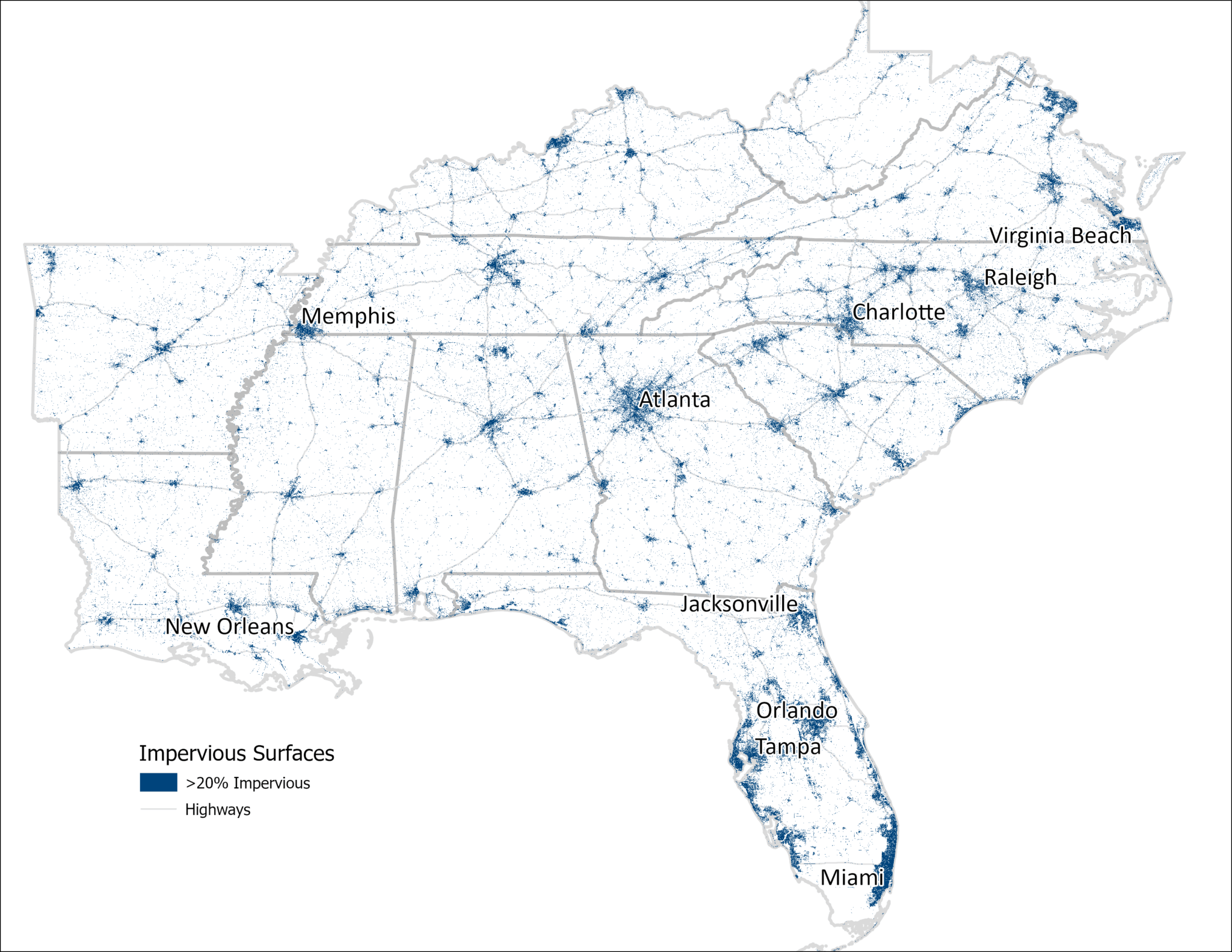

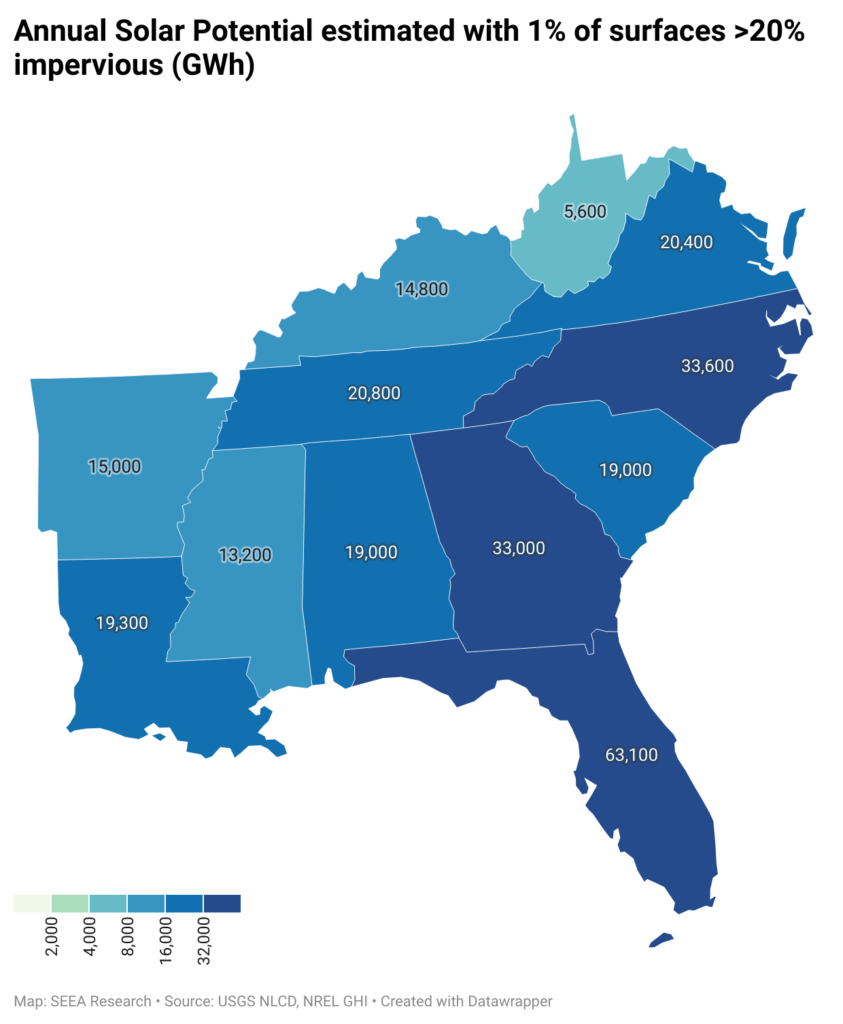

Solar Potential of Impervious Surfaces in the Southeast

Installation of solar photovoltaic panels on even a small fraction of the impervious surfaces in the urban environment in the Southeast could provide a significant boost in energy generation.

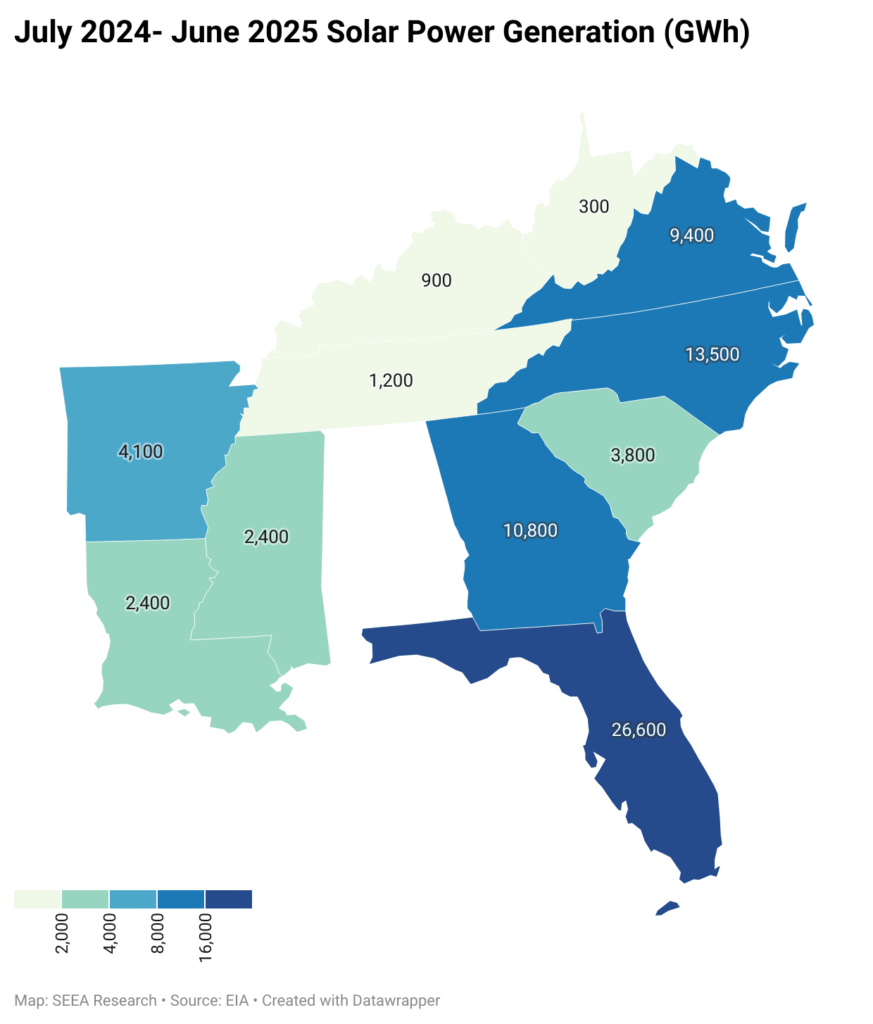

As solar photovoltaic technology has become increasingly affordable for electricity generation, both utility-scale and small-scale solar power (<1MW) have grown. Between June 2024 and June 2025, in the entire United States, solar power generation grew 25.4%. In the Southeast, Arkansas, Kentucky, Louisiana, and Mississippi all increased their solar power generation over 90% during the same period. This increase has raised questions about land use and the potential conversion of agricultural land into solar farms.

While the land area in use for solar power is a tiny fraction of the land in use as farms in the Southeast (and nationwide), it is worth considering what is the potential for solar power on land that is already in use. When land is covered with surfaces such as parking lots, buildings, sidewalks, and roads, water cannot effectively soak into the ground. When it rains, such impervious surfaces limit access to natural infiltration in the soil, which can lead to increased water runoff, flooding, and concentration of pollutants in streams and drinking water. Since solar panels are also impervious surfaces, placing them on rooftops and parking surfaces that are already in the built environment makes dual use of existing structures for supplementary power generation. In this map of the month, we highlight where the impervious surfaces are located in the Southeast and estimate the potential solar power generation capacity of these locations.

Using data from the U.S. Geological Survey National Land Cover Database, we determined the fractional surface area that is covered with artificial structures in our region. We sum the areas where the fractional impervious surface is greater than 20%, yielding 75,000 km2 of land area, shown in navy blue on the map below. Not surprisingly, the highlighted areas are primarily in urban areas and along major highways.

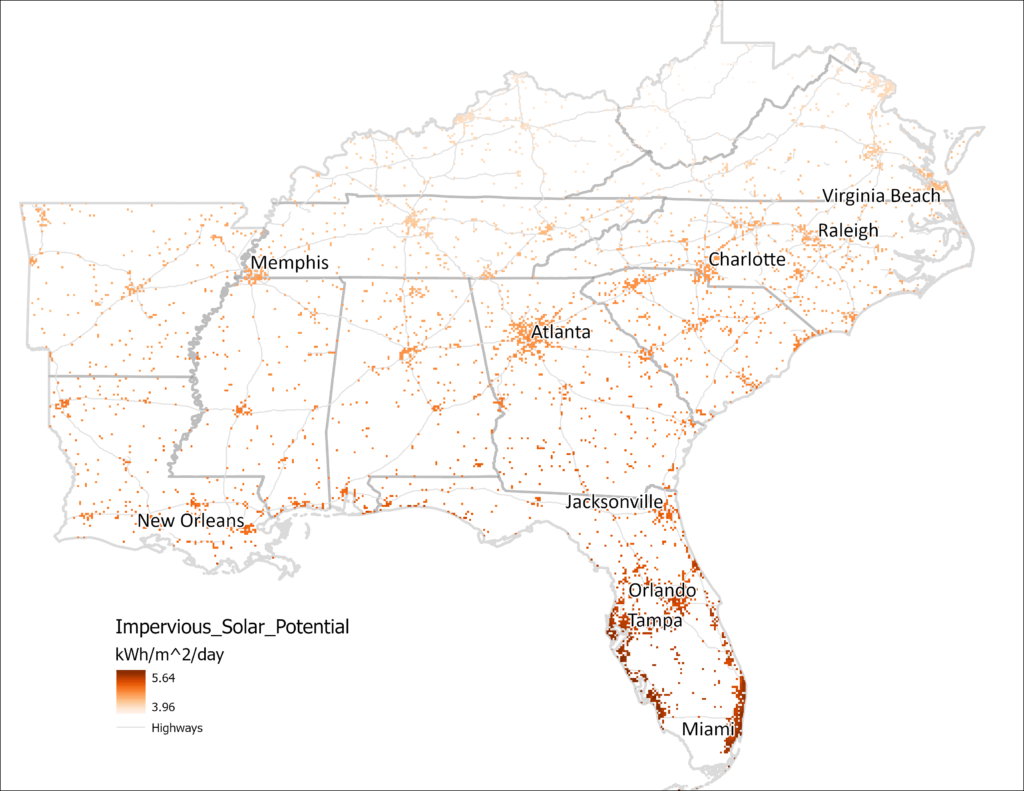

The National Renewable Energy Lab (NREL) provides estimates of the average potential for solar power using global horizontal irradiance (GHI), which is measured in kilowatt-hours (kWh) per square meter per day. In the Southeast, GHI varies approximately from 4-6 kWh/m2/day. If solar panels were deployed over even 1% of the (>20%) impervious surfaces on this map (185,000 acres or 750 km2), at 4 kWh/m2/day, with 20% panel efficiency, the region could generate 219,000 GWh annually. Compare this with 75,300 GWh already generated by solar facilities in these states between July 2024 and June 2025, this one percent could increase the region’s solar power contribution by a factor of 2.8, with enough to power 20 million homes, or approximately half of homes in these states.

Not all impervious surfaces are suitable for installation of solar panels, but adding panels to even a small percentage of the existing infrastructure could provide a significant additional source of electric power, without covering new land at all. This dual use of some of the urban built environment is equivalent to 400 farms at the 2022 average size of 463 acres each. Furthermore, solar panels on existing rooftops or parking lots provide artificial shade that can help to reduce the urban heat-island effect, offset peak electric power demand in urban areas where there is a lot of daytime power demand, and are more readily tied into existing grid infrastructure than panels in more rural areas.

August Map of the Month

By Laura Diaz-Villaquiran

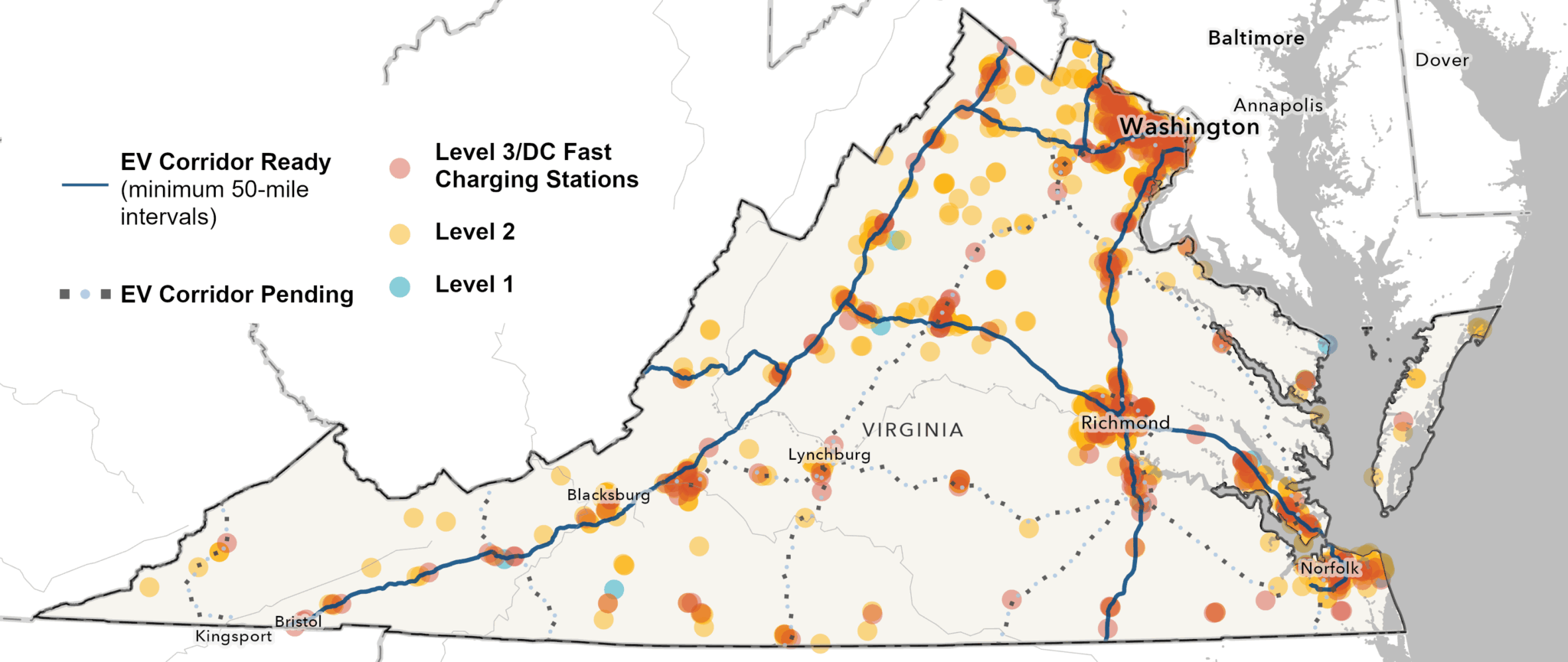

Public EV Charging Stations in the Commonwealth

Source: U.S. Department of Energy, Alternative Fuels Data Center

The U.S. EV charging network has grown from 5,070 EV charging ports in 2011 to more than 184,000 in 2023, a 36-fold increase in just over a decade. This rapid expansion is vital for consumers, who depend on reliable and accessible charging infrastructure. As the U.S. Department of Energy’s Alternative Fuels Data Center (AFDC) explains, while most drivers begin by charging at home or at fleet facilities, public and workplace stations, “help bolster market acceptance by offering more flexible charging opportunities at commonly visited locations.”

This Map of the Month highlights publicly available EV charging stations in the Commonwealth of Virginia, along with the state’s EV-ready and pending fuel corridors. Under the National Electric Vehicle Infrastructure (NEVI) program, previous guidance stated that stations must be located within 50 miles of one another to qualify as corridor-ready, but that has changed.

Virginia’s network is steadily taking shape. Today, the Commonwealth is home to 1,838 public EV charging stations, with a total of 5,316 charging ports. Of these, 344 are Level 3 direct-current (DC) fast charging stations, the highest-capacity chargers available. These stations make long-distance EV travel increasingly practical and reliable, with the AFDC noting that “DC fast charging equipment (typically a three-phase AC input) enables rapid charging along heavy traffic corridors at installed stations at power outputs up to 500 kW.”

Virginia’s interstates serve as a pass-through from the South to the Midwest and the Northeast, making this growing network especially significant for regional and national EV travel. Our map also indicates that charging “hot spots” are concentrated in Virginia’s urban areas, such as Arlington, Alexandria, Richmond, Norfolk, Lynchburg, and Blacksburg. These clusters highlight the state’s progress while underscoring the need to expand access in rural communities.

On February 6, 2025, the Federal Highway Administration (FHWA) announced a pause on the current NEVI Formula Program. But even with this pause, Virginians still have access to a wide range of residential and non-residential utility incentives that are helping to accelerate EV adoption:

- Appalachian Power offers time-of-use (TOU) rates for EV charging, rebates for Level 2 charging station purchases, and infrastructure support.

- Dominion Energy provides rebates and pilot programs for both residential and non-residential charging stations.

- Northern Virginia Electric Cooperative (NOVEC) and Rappahannock Electric Cooperative (REC) both extend TOU rate incentives to residential customers.

- Tennessee Valley Authority (TVA) supports non-residential adoption through rebates for DC fast charging station purchases, installation incentives, and deployment pilot programs.

Together, these programs make it easier for households and businesses to invest in charging infrastructure and alternative fuel options. For the most up-to-date information, the Alternative Fuels Data Center maintains a comprehensive directory of incentives, laws, and regulations available in Virginia.

July Map of the Month

By William D. Bryan, Ph.D.

The federal Low Income Home Energy Assistance Program (LIHEAP) is a lifeline for millions of Americans. Since 1981, this program has helped low-income households keep their lights on and remain safe during extreme weather through bill assistance, crisis intervention, and funding for weatherization improvements.

Despite its demonstrated impact, LIHEAP faces an uncertain future. The White House proposed eliminating the program in its FY26 budget recommendations, and the entire staff at the U.S. Department of Health and Human Services (HHS) responsible for administering LIHEAP was terminated this April. Ending this program will leave millions of households with no stopgap for unaffordable energy and extreme weather, with ripple effects on states, utilities, and ratepayers in the South.

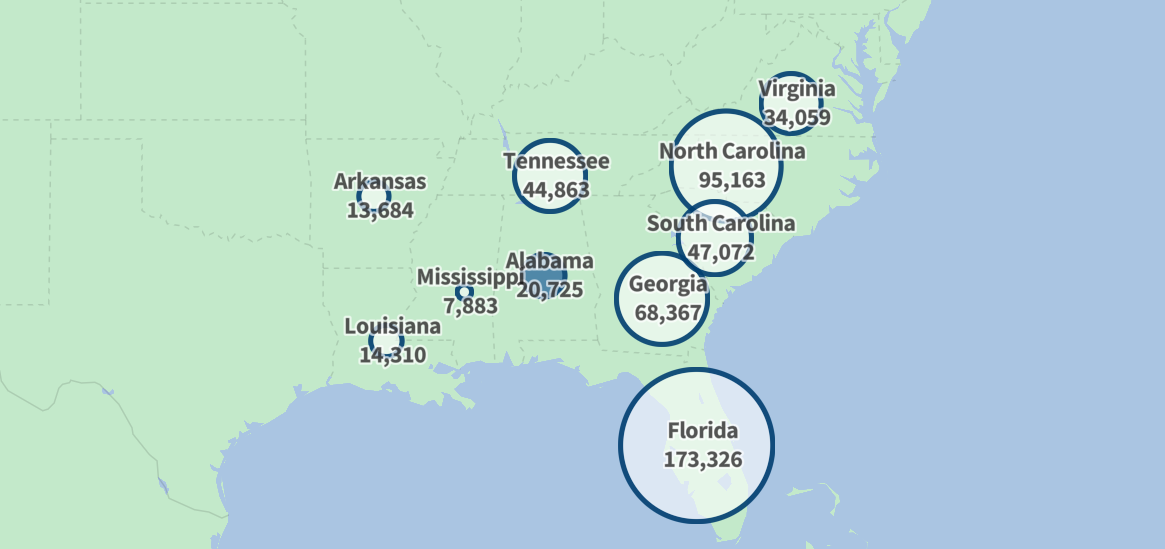

Using data from the LIHEAP Data Warehouse, this month’s visualization explores the significant impact this program has had on the Southeast. Over the past decade, LIHEAP has supported 10.3 million households in the Southeast, and more than 52 million households nationally. In FY24, this made up nearly 15% of households at or below 150% of the federal poverty level across the region. Almost three-quarters of Southern households served (7.75 million) include at least one resident in a vulnerable age group (60+ or under 5 years old) or with a disability.

Though benefits vary by state, LIHEAP provides emergency assistance for households who struggle to afford their energy bills and may face the disconnection of essential energy services – an event that can contribute to heightened health and safety risks, potential housing displacement, and strained household finances. Since 2016, this assistance has prevented or resolved disconnections for 4.6 million households in the South. As this month’s chart shows, Kentucky and North Carolina lead the region with the highest number of households who were able to avoid disconnection or have their service restored thanks to LIHEAP, followed by Alabama. In Kentucky alone, 1.25 million households have avoided disconnection entirely or been reconnected thanks to LIHEAP – more than in any other state in the nation.

Although LIHEAP is primarily known as a bill assistance program, states can allocate a portion of their funding to support weatherization efforts that permanently reduce energy bills. Through the U.S. Department of Energy’s Weatherization Assistance Program (WAP), LIHEAP has funded the weatherization of 220,127 households in the South since 2001, allowing WAP providers extend their reach and serve more households with energy- and cost-saving home improvements. As the chart below shows, five states – Arkansas, Kentucky, South Carolina, Virginia, and West Virginia – have reached their maximum contribution to weatherization, though they can exceed this 15% allocation through a waiver.

The elimination of LIHEAP would remove a vital backstop for financially insecure households, making it harder for millions of people across the Southeast to catch up on overdue energy bills. In FY24, the average energy burden for LIHEAP recipients in the South was 14.5% of household income, well over the 12.4% national average and nearly two-and-a-half times the 6% threshold considered affordable. A 2018 survey conducted by the National Energy Assistance Directors Association (NEADA) underscored the difficult tradeoffs that LIHEAP recipients often have to make to maintain access to energy: 36% went without food for at least one day to save money for utility bills, 41% skipped medical or dental care, 30% resorted to heating their home with an oven or stove, and a quarter kept their homes at unhealthy or unsafe temperatures. Trade-offs like this were not always enough to make bills affordable, and 13% of LIHEAP recipients took out high-interest payday loans to cover utility bills, deepening their financial precarity.

Besides the direct impacts on households receiving assistance and efficiency investment, the elimination of LIHEAP is likely to increase energy costs for all ratepayers. When customers fall behind on their bills and face disconnection, utilities incur “bad debt” costs that are often passed along to consumers through higher energy rates. In 2024, utilities nationwide faced $17.4 billion in bad debt from customers with substantial arrearages or disconnections due to nonpayment, an 8.4% increase from the previous year, which NEADA attributes to significant cuts in LIHEAP funding. Although this was less than during the peak of the COVID-19 pandemic, bad debt remains a challenge amid historic demand levels that are putting upward pressure on rates. Without access to LIHEAP, the 1.2 million households in the Southeast who successfully resolved utility disconnections last year will have no recourse, likely increasing bad debt and requiring utilities to invest in energy efficiency, bill management, and payment assistance programs to keep arrearages under control.

LIHEAP is a critical safeguard serving a large population in the Southeast while helping to mitigate rate increases caused by utility bad debt. In FY24, LIHEAP assisted 1.1 million households in the region – outpacing all other federal, state, local, and utility assistance and weatherization programs. Beyond providing immediate bill assistance, LIHEAP also expands access to weatherization services that permanently reduce energy consumption, offering a long-term path to lower energy bills. The elimination of LIHEAP threatens to put energy affordability further out of reach for millions of households across the Southeast, driving up costs for all ratepayers, exacerbating financial hardship, and increasing risks of utility disconnections at a time when rising energy costs and extreme weather already strain household budgets.

*Stay tuned for SEEA’s forthcoming policy brief on LIHEAP for a deeper dive into the program’s impact on the Southeast. Please reach out to Will Bryan, Director of Research, for more information.

June Map of the Month

By Elizabeth Willis

Map: Southeast Energy Efficiency Alliance (SEEA), Source: U.S. Census Bureau, U.S Department of Energy

Residential construction in the Southeastern United States has ebbed and flowed over the past three decades, shaped by economic cycles, population shifts, and policy changes. Among these influences, statewide updates to building energy codes have attracted growing attention. Do they meaningfully affect construction activity? Or are their effects overstated?

This month’s map looks at the relationship between residential building activity and the implementation of statewide energy codes across the region. As the Southeast continues to experience high rates of population growth and demand for affordable, resilient housing, policymakers and industry professionals should consider how residential energy efficiency measures can be advanced without constraining development.

Using information from the U.S. Census Bureau’s Building Permits Survey (BPS), this month’s map displays the annual number of new, privately-owned, single-family residential building permits issued in each Southeastern state from 1995 through 2024. Overlaid on this time series are blue-flashing indicators marking the years when each state adopted a new or updated version of its residential building code. By visualizing these two datasets together, the map offers a regional snapshot of how construction activity has evolved over time—and whether building code updates influence permit volumes.

The Building Permit Survey (BPS) data used here is publicly available through the U.S. Census Bureau and represents an estimate of new residential building permits. It does not include information on renovations, remodeling, or additions. The intent of this visual is to observe large-scale trends in Southeastern states and contextualize them within the timeline of code adoption.

Most Southeastern states have updated their building energy codes at least once – often multiple times – since 1995. Yet in nearly all cases, these updates do not correspond with sharp declines in new residential construction. In fact, building permit volumes often continue to rise even after major code adoptions. The one clear and dramatic exception is the 2008 housing market crash, which triggered a steep regional decline in permit numbers. However, that downturn was rooted in macroeconomic instability, not regulatory change or code updates.

State-by-state patterns provide further texture. Florida, for instance, consistently shows the highest permit volumes in the region, driven in part by sustained population growth. North Carolina stands out for its triennial code update cycle, which has not hindered its steady stream of residential development. Even in states that have adopted relatively stringent codes – such as Georgia or Virginia – there is no evidence to suggest a long-term construction suppression following code implementation.

The data suggests that these impacts do not translate into a slowdown of regional construction. Instead, residential construction activity remains largely robust, even through multiple rounds of code revision. The dominant influences on residential construction activity are market-driven: availability of financing, consumer demand, labor supply, and broader economic health.

Ultimately, statewide energy code updates, though sometimes perceived as a potential hindrance to development, have not restrained residential construction in practice. Policymakers and industry professionals should consider this perspective when evaluating future code proposals and updates. While regulation warrants scrutiny, the data in this map suggests that energy codes have largely coexisted with a robust, responsive housing market in the Southeastern United States. Alongside sustained patterns of residential growth, building energy codes are a key tool for advancing public health, safety, and affordability. By establishing minimum standards for ventilation, insulation, and mechanical systems, these codes improve indoor air quality, reduce risk of respiratory illness, increase comfort, and lower energy burdens. Over the lifespan of a home, they also yield significant cost savings for residents by improving efficiency and reducing utility bills (NEEP, 2021).

SEEA has previously published The Economic Impact of Commercial Energy Codes in the Southeast, which found that stronger codes do not significantly hinder commercial construction. You can access the full report here.

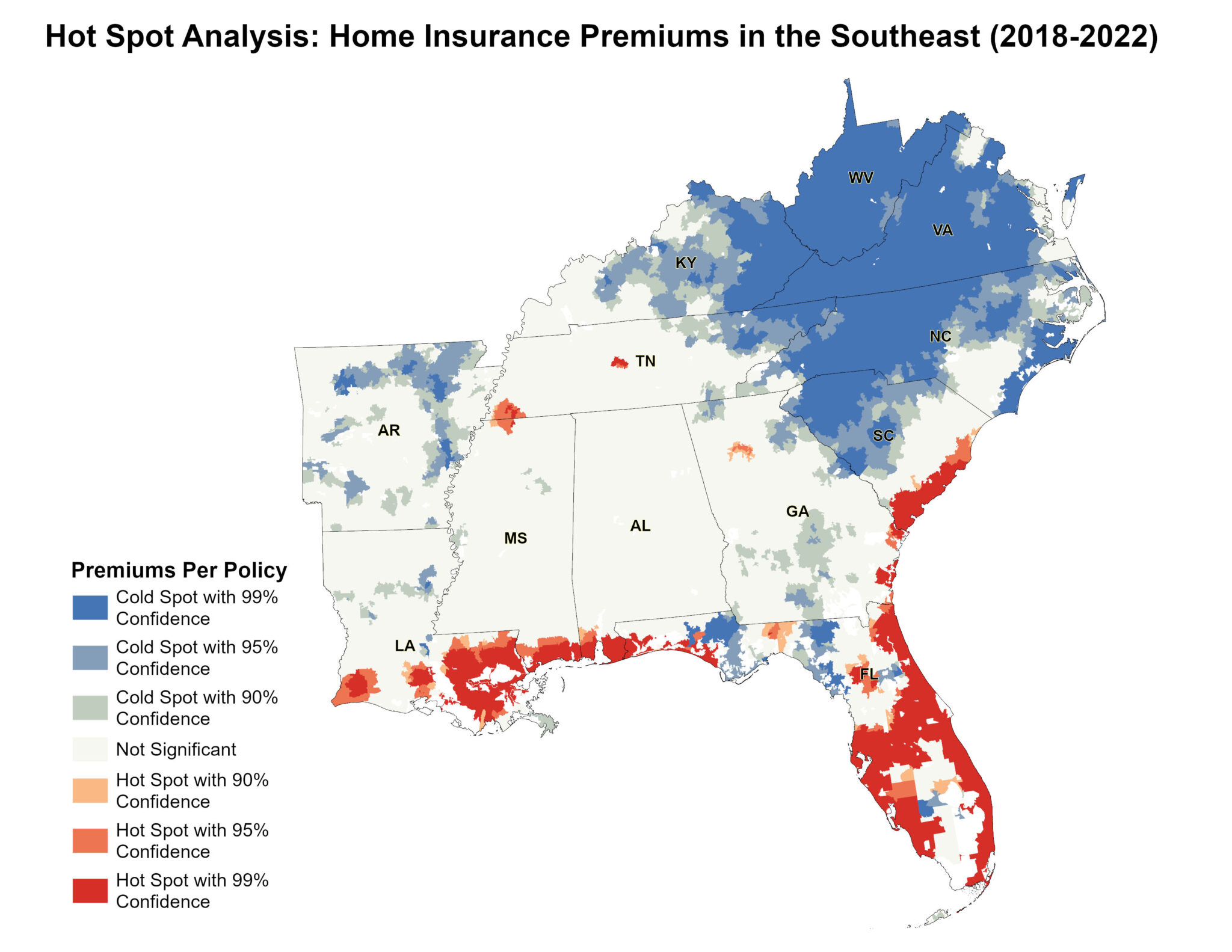

March Map of the Month

By Laura Diaz-Villaquiran

Source: Federal Insurance Office, U.S. Department of Treasury.

Home insurance costs are rising across the Southeast, threatening housing affordability for homeowners and renters alike. With the frequency and severity of climate-related disasters increasing, insurers are passing higher costs onto policyholders. Between 2018 and 2022, home insurance premiums written by the top 10 insurers in the region surged from $9.4 billion to $14.3 billion. Florida and Louisiana have been hit particularly hard and have some of the highest premium increases and non-renewal rates in the country.

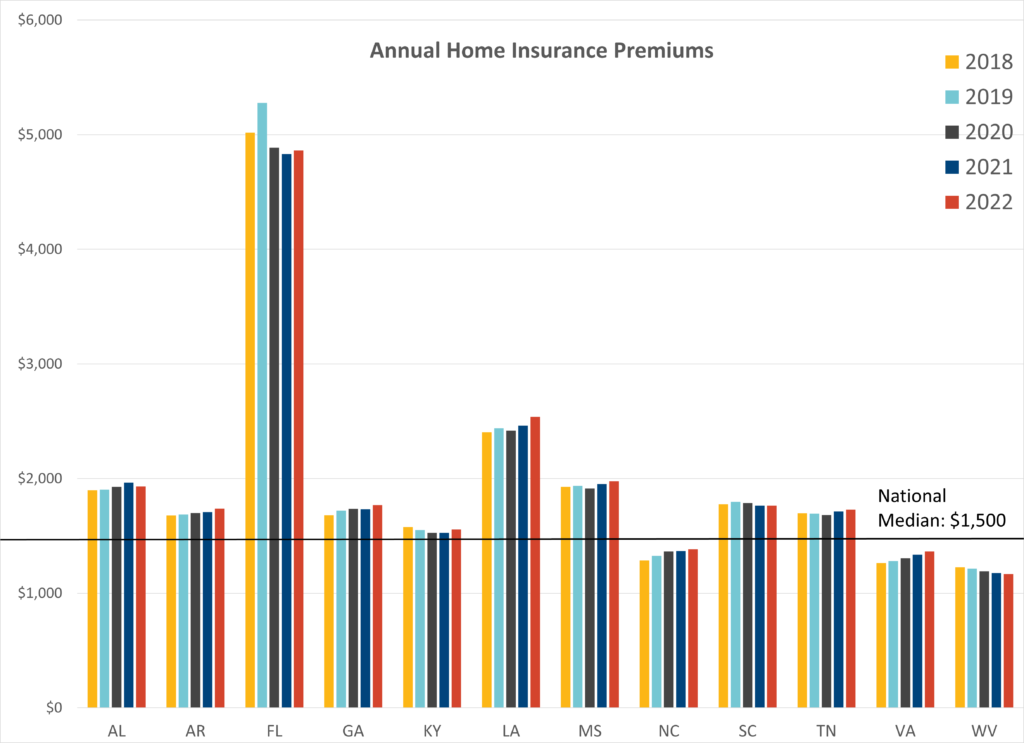

Using data from the same period provided by the U.S. Department of the Treasury, this month’s map highlights spatial patterns of home insurance costs across the Southeast through a geographic hot spot analysis. This dataset consists of comprehensive home insurance policies, which make up 85% of the home insurance market in the U.S. A hot spot analysis is a geospatial method used to detect statistically significant clusters of high or low values compared to surrounding regions. Insurance rates are calculated based on location, home value, and risk exposure. Nationally the median cost of home insurance was $1,500, while the average premium for that same period was $1,900. For the Southeast, the median premium was $1,600. See the recent average annual home insurance premiums for Southeastern states below:

This month’s map highlights areas where insurance premiums are high and cluster with other high values, with 99% confidence. Hot spots are concentrated along the Gulf and Atlantic coasts, while areas with lower premiums, also with 99% confidence, are primarily found further inland and north, in states like Kentucky, Virginia, West Virginia, and western North Carolina. In climate-vulnerable states like Florida, where extreme weather events have led to frequent insurance payouts, insurers have hiked premiums to remain solvent.

Beyond rising premiums, home insurance availability is shrinking as insurers withdraw from high-risk areas. Between 2018 and 2022, the average non-renewal rate in the Southeast (1.43%) was 38% higher than the national average (1.04%). This trend accelerated in 2023, with North Carolina and South Carolina experiencing sharp increases in non-renewals. Florida had the highest share of non-renewals, with insurers citing hurricane-related losses as the primary reason for exiting the market.

For homeowners, insurance is a necessity. Lenders require coverage to secure mortgages, and without it, banks can foreclose on homes. For renters, rising insurance costs can translate to higher rents, as landlords pass increased premiums onto tenants.

A 2025 First Street report found that in many Southeastern cities, insurance costs are outpacing home price growth. Traditionally, the region offered lower housing costs, but the risk of extreme weather has pushed insurance from 8% of mortgage payments in 2013 to more than 20% by 2022. Homeowners in Miami (322%), Jacksonville (226%), Tampa (213%), and New Orleans (196%) have seen the steepest premium increases in the region.

As the Southeast braces for the impact of rising sea levels, extreme heat, and increasing hurricane activity, planning for resilience is more critical than ever. Mitigation strategies will play an essential role in ensuring long-term housing is affordable and resilient. Improving residential energy efficiency can play a role in enhancing the resilience of housing during extreme weather and improving housing affordability to offset premium increases. Strengthening building codes, expanding access to energy efficiency, and investing in resilient infrastructure will be key in offsetting rising insurance costs and protecting homeowners and renters across the region.